View:

April 25, 2024

U.S. March Pending Home Sales bounce follows sharp February rise in Existing Home Sales

April 25, 2024 2:14 PM UTC

March has seen a stronger than expected 3.4% increase in pending home sales. Normally pending home sales lead existing home sales but in this case we appear to be seeing a catch up with strength in February existing home sales.

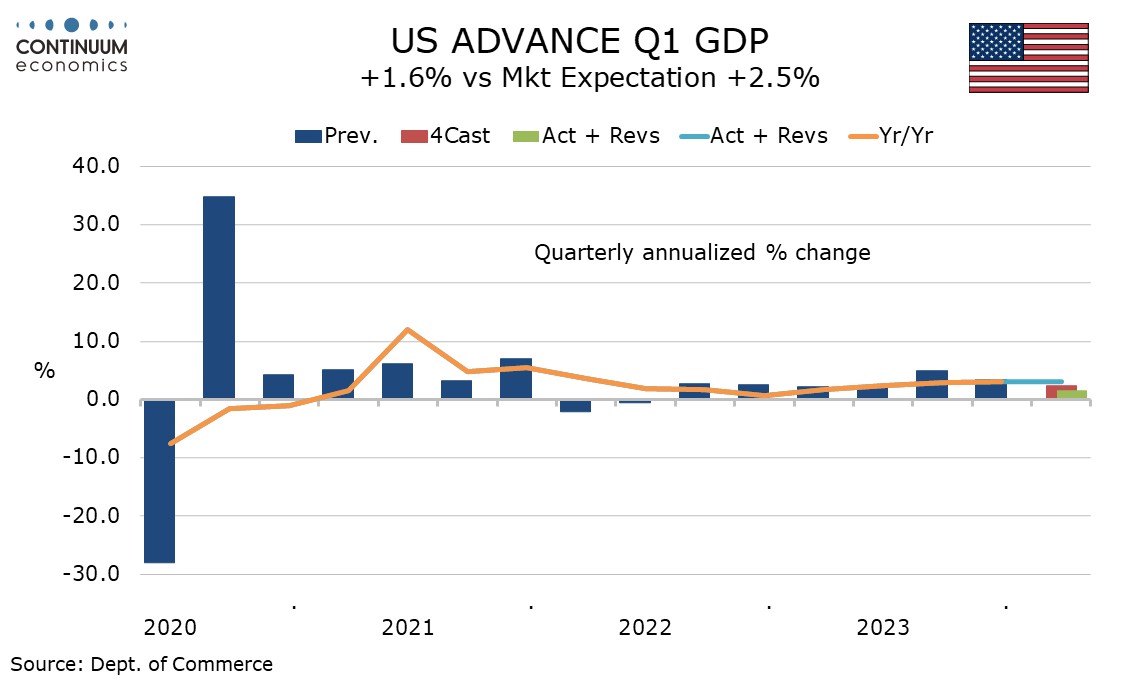

Q1 U.S. GDP Slows on Imports and Inventories, Core PCE Prices Stronger on the Quarter

April 25, 2024 1:14 PM UTC

Q4 GDP has come in weaker than expected at 1.6% annualized but with a stronger than expected 3.7% annualized increase in the core PCE price index. Weaker inventories and stronger imports are the main reason for the GDP slowing so the data is not a clear signal of underlying weakness. Lower initial (

Norges Bank Preview: Nothing New to Note?

April 25, 2024 9:29 AM UTC

Surprising few, the Norges Bank Board is very likely to leave its policy rate at 4.5% for a third successive meeting when it gives it next verdict on May 3. It is also likely to retain the thinking first aired at the December meeting, namely the ‘policy to stay on hold for some time ahead’ rhe

JPY flows: JPY weakness intensifies, intervention possible, but...

April 25, 2024 7:07 AM UTC

JPY weakness intensified overnight and increased the potential for intervention. This may be seen in the next few days, and the JPY does have potential to rally sharply given the huge real decline in recent years. But a turn higher in risk premia looks necessary to trigger a long term reversal of cu

BoJ's Intervention and its impact

April 25, 2024 6:24 AM UTC

In the period of time when JPY significantly weakens or strengthens, BoJ will intervene in the FX market either through verbal or actual intervention. As JPY weakened significantly in the past months, once again we found ourselves in the proximity of FX intervention with unknowns for anonymity is ke

April 24, 2024

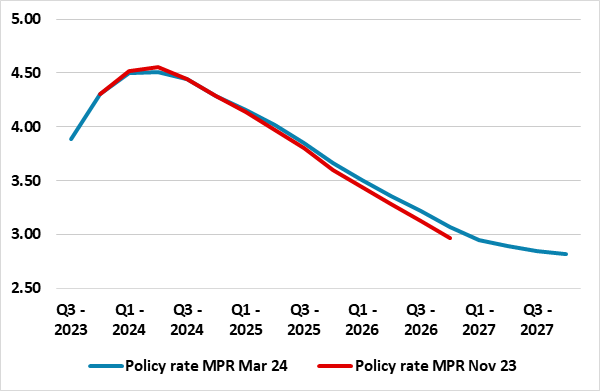

Bank of Canada Minutes Look to Gradual Easing, Divided on When to Start

April 24, 2024 6:44 PM UTC

Bank of Canada minutes from the April 10 meeting confirm a greater confidence on inflation falling, though there is disagreement within the Governing Council over when policy easing will become appropriate. There was agreement that easing would probably be gradual given the risks to the outlook and

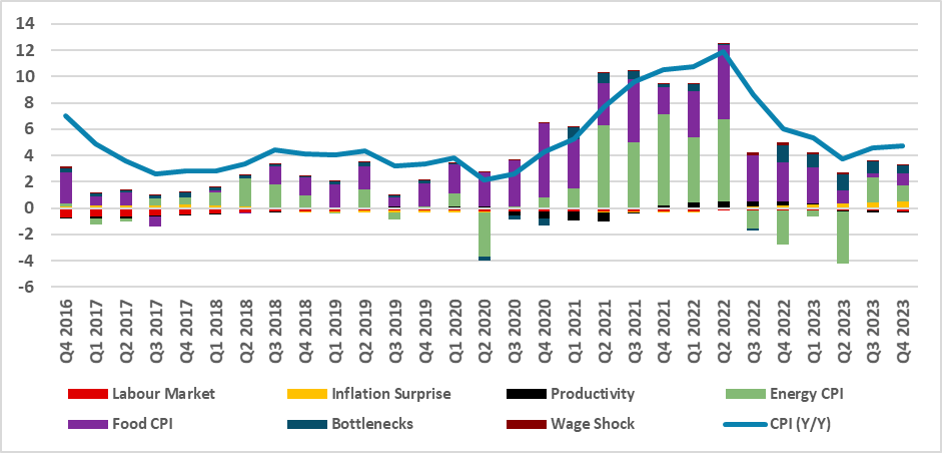

Brazil: Wage Inflation Will Likely Not Be a Big Deal

April 24, 2024 3:19 PM UTC

Our analysis delves into recent trends in the Brazilian labor market, focusing on CPI and wage inflation. Utilizing a model akin to Ghomi et al. (2024) and Blanchard and Bernanke (2023), we dissect recent spikes in wage inflation and CPI growth. Notably, our findings suggest that recent wage spikes